1: Covid: moving toward a new normal?

COVID-19 is (hopefully) in the process of transitioning from a pandemic disease to an endemic disease – a nuisance, rather than the devastator we faced in 2020.

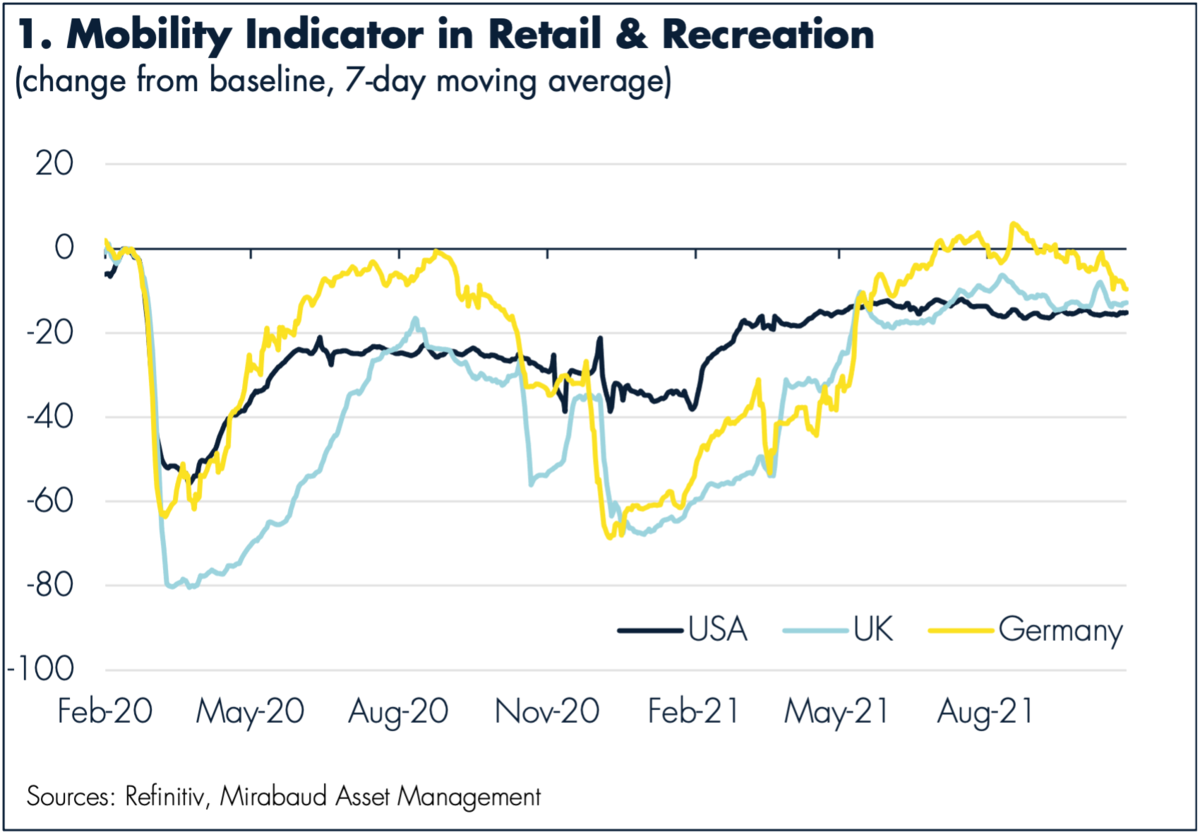

Here we see one of the key metrics indicating just how much the virus dented activity in the UK, the US and Germany. Despite wildly differing policy responses to the virus, 2021 is ending with all three markets’ retail and recreation sectors returning to something approaching ‘normal’.

However, we should note that at the time of writing the full impact of the Omicron variant remains uncertain.

2: A tale of two pandemics

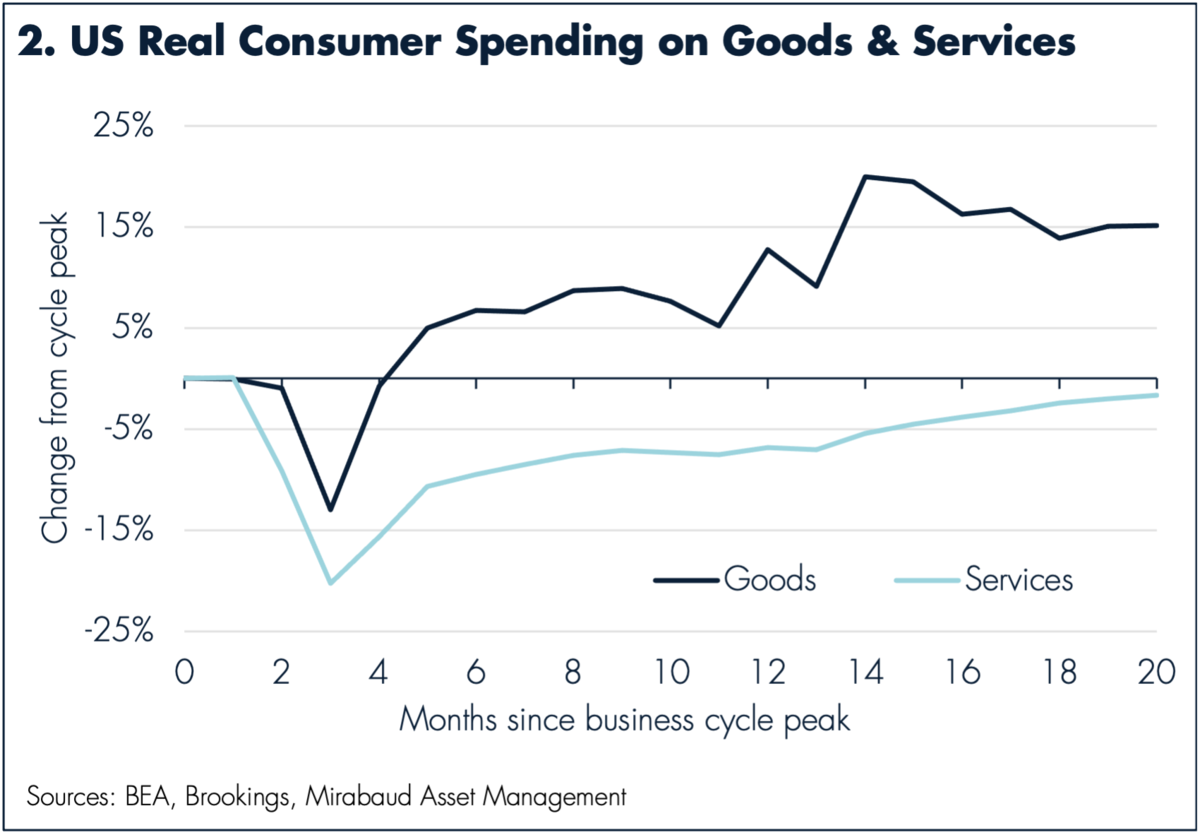

One of the more striking impacts of the pandemic was the radical divergence in consumer spending between the two most basic categories: goods and services.

In short, as people stayed home and faced fewer opportunities for discretionary spending, spending on anything that could be delivered soared as consumers felt flush.

Meanwhile, spending on services that actually required the consumer to be physically present collapsed, for obvious reasons.

Again, though, in the US we are currently seeing spending on services return to a pre-Covid baseline, even if spending on goods remains high. How long this ‘lockdown dividend’ of consumers spending their accumulated savings will last remains to be seen.

3: Message in a bottleneck

Cheap shipping has been one of the core assumptions of our globalised world economy for more than 40 years, and the exceptional market conditions we have seen this year represent one of the first real challenges to this model.

If 2020 saw one of the great demand shocks in history, 2021 an equal and opposite shock as key markets emerged from lockdowns. Demand shot up, but global supply chains and infrastructure struggled to meet the challenge as they faced their own difficulties.

This means that shipping costs are now far higher than they have been for years, which is having complex and unpredictable effects elsewhere in the global economy. When this will ease, and to what extent, remains to be seen.

4: Inflation - back from the dead?

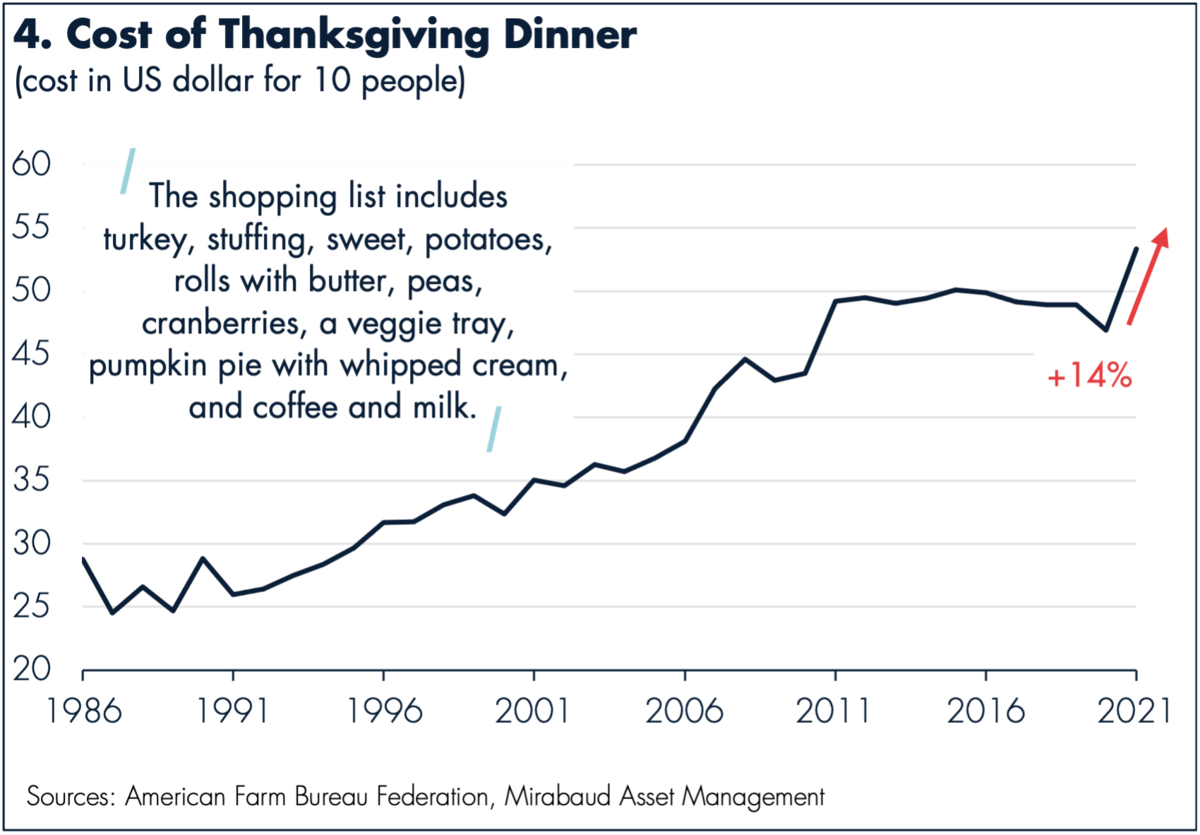

Inflation – another question thought ‘solved’ until recently – returned to the headlines in 2021.

It’s a macro idea that consumers can actually see in their everyday lives too, as we can see below in the hefty jump in the cost of Americans’ Thanksgiving dinners:

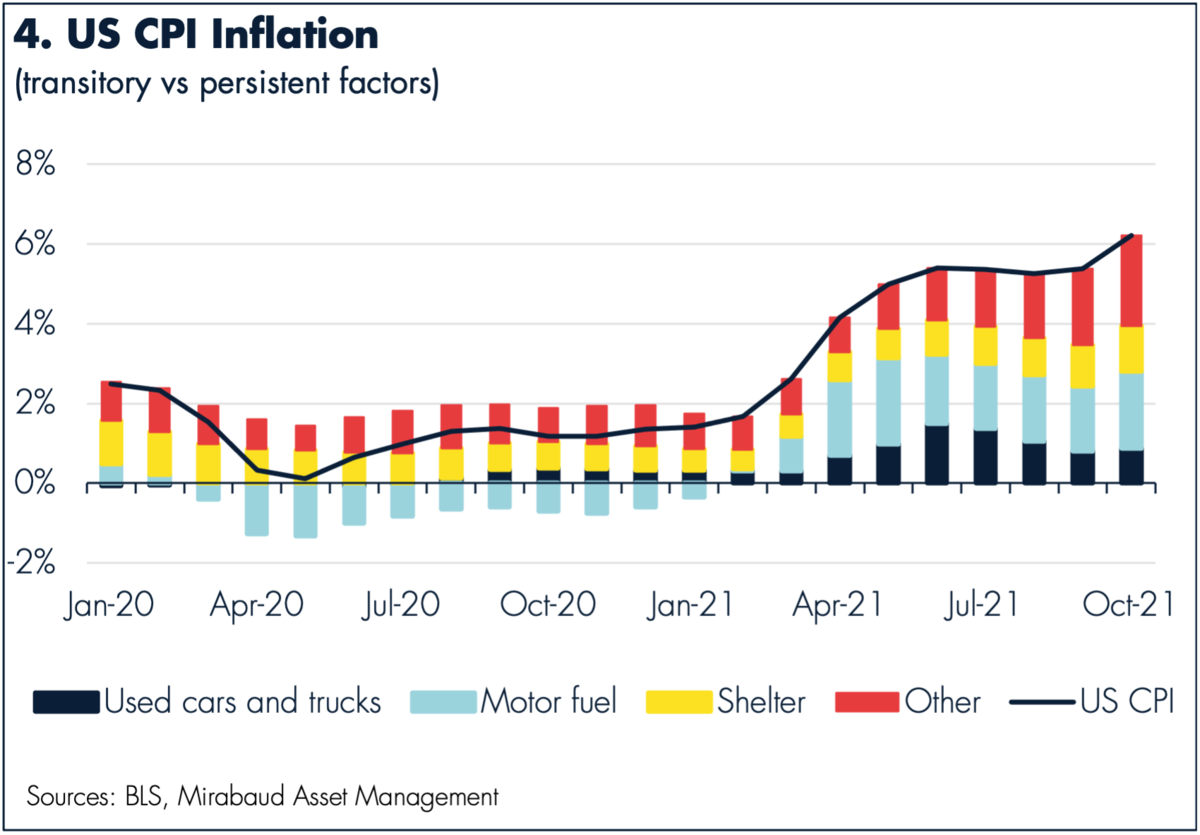

There’s good news and bad news.

The good? The factors driving up prices at present are not fundamental, and should ease over the course of 2022.

However, prices for services did not fall despite plunging demand over the last two years. As we move into the new year, they too are likely to experience significant inflation.

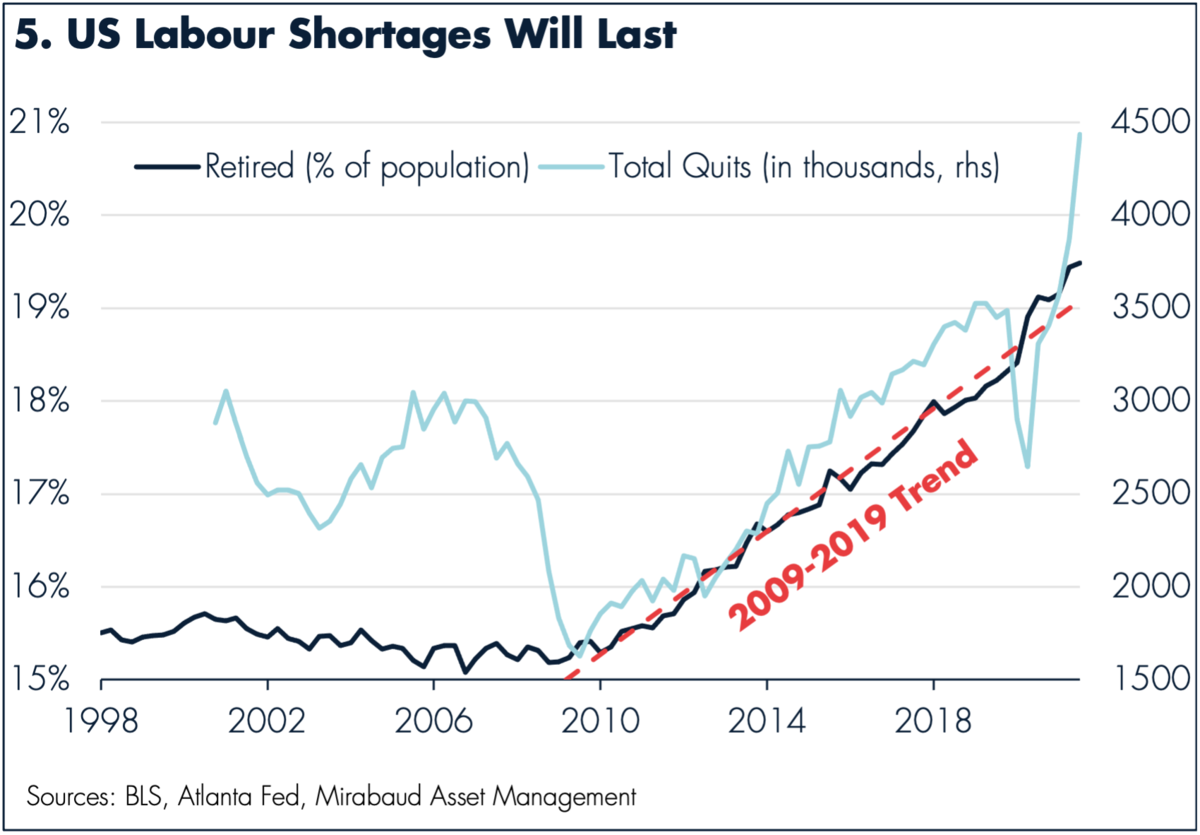

5: The ‘great resignation’

The pandemic led many of us to rethink what we held most important in our lives, and 2021 saw this played out in the American labour market.

As many US workers either leave work altogether or seek a more acceptable work/life balance, it is translating into high demand for workers in the service economy not being met as the overall labour supply shrank. This is putting upward pressure on wages that is unlikely to ease any time soon.

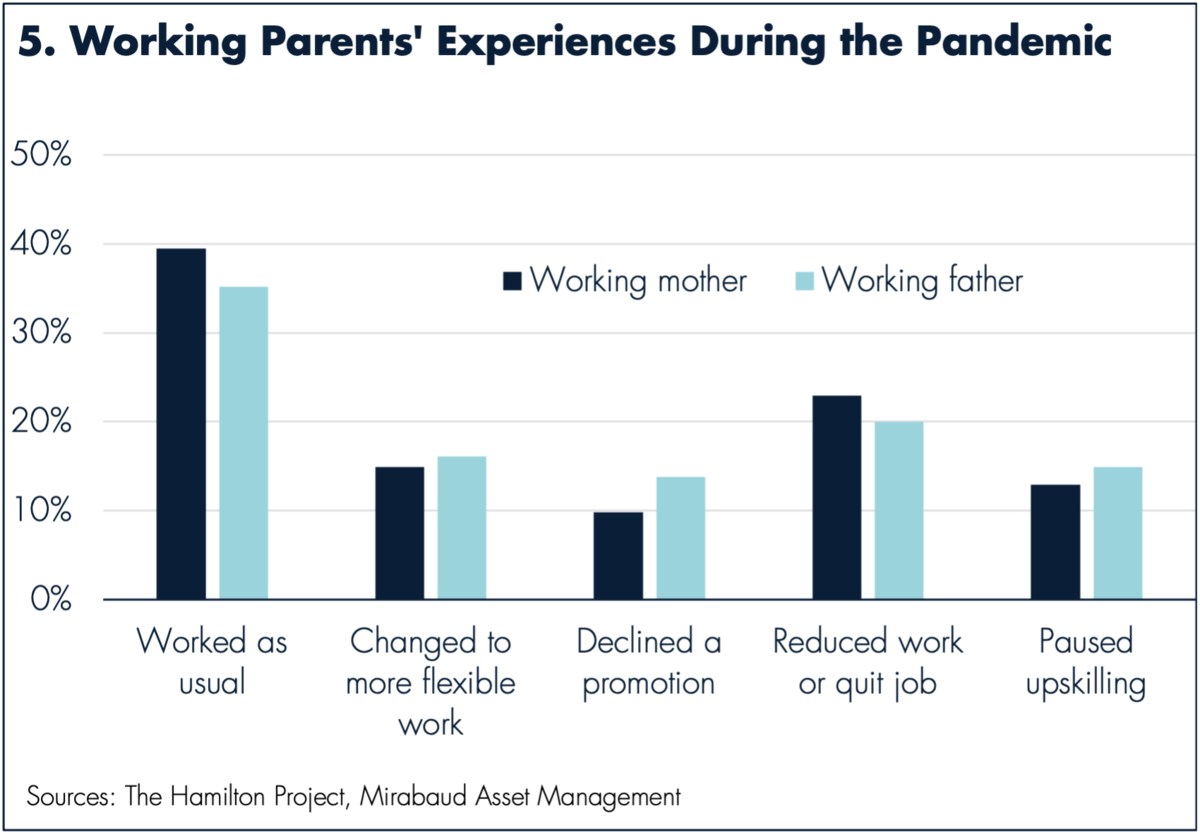

It’s also worth pointing out that, much as the impact of Covid was highly determined by one’s socioeconomic circumstances. ‘The great resignation’ is manifesting itself in very different ways across different segments of American society, as we can see in the gender breakdown below:

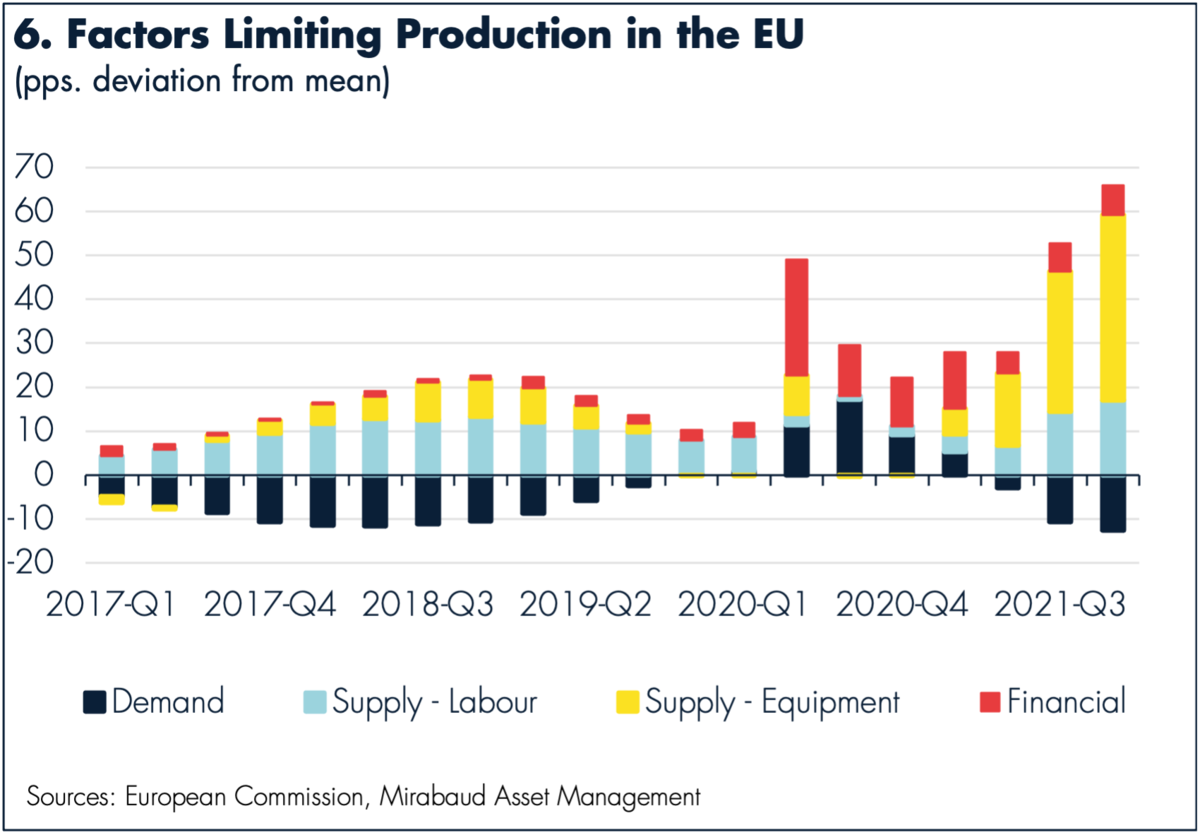

6: Europe not exempt from shortages

The EU is not exempt from the issues facing the rest of the world.

Although labour isn’t the issue it is across the Atlantic, shortages of materials and equipment are limiting the manufacturing sector’s recovery, even as demand remains solid.

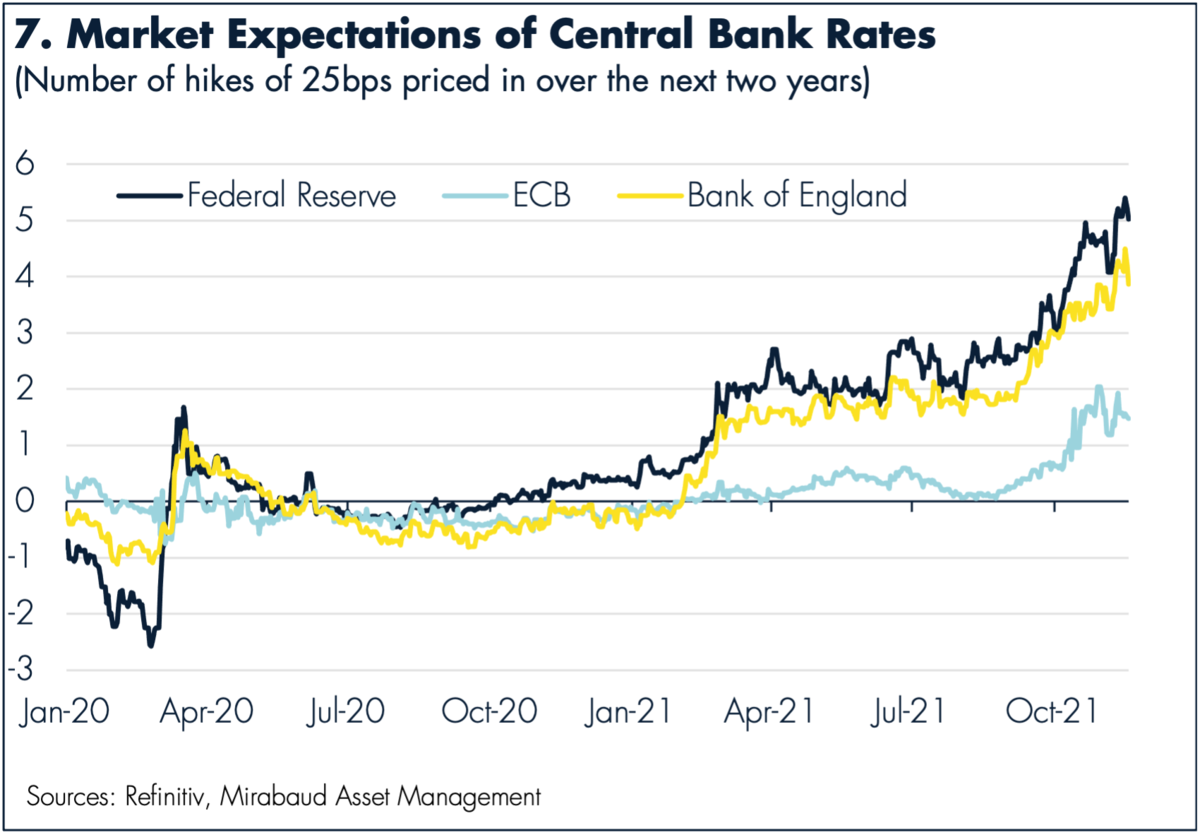

7: Market consensus on base rate hikes

Rising inflation in developed markets’ services sector is highly likely to drive central banks to tighten monetary policies, with the market pricing in several hikes in the coming years.

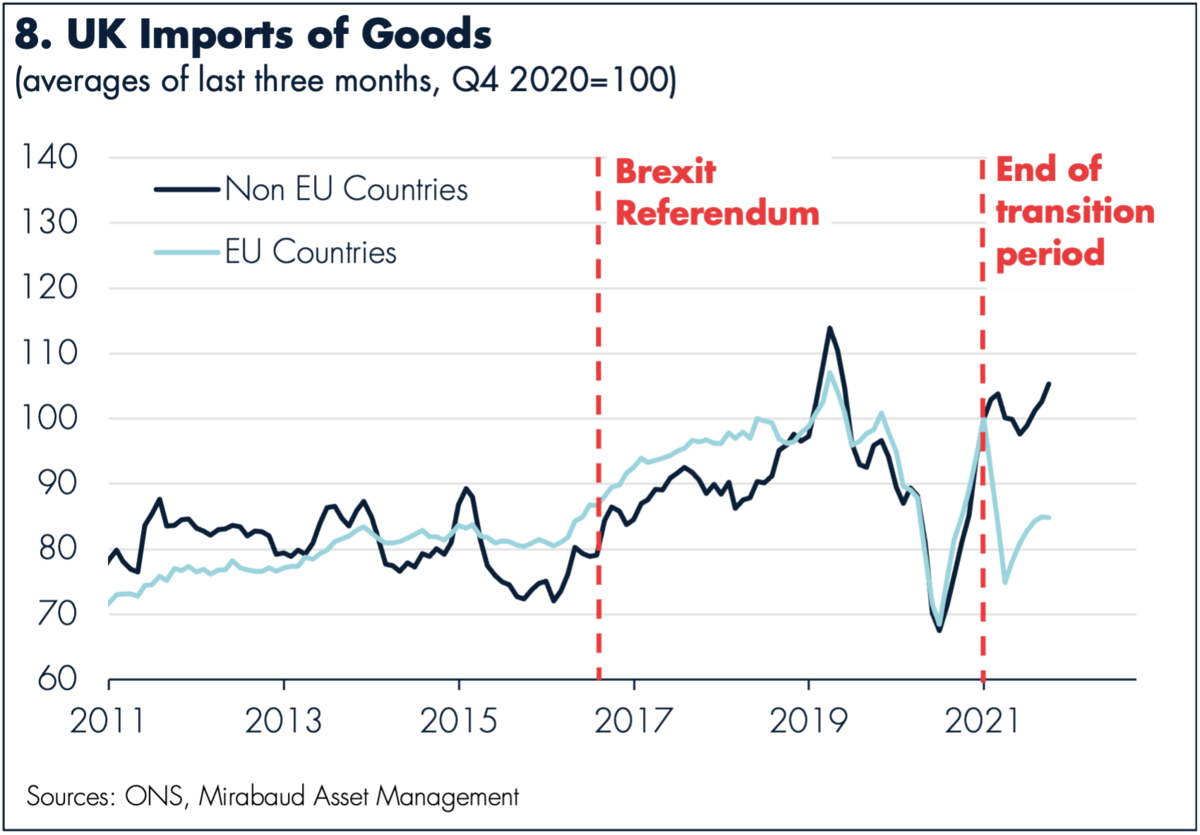

8: From Brexit dream to Brexit reality

In early 2021, the UK finally completed its formal withdrawal from the EU.

As we can see, imports from the EU immediately collapsed, only to partially recover.

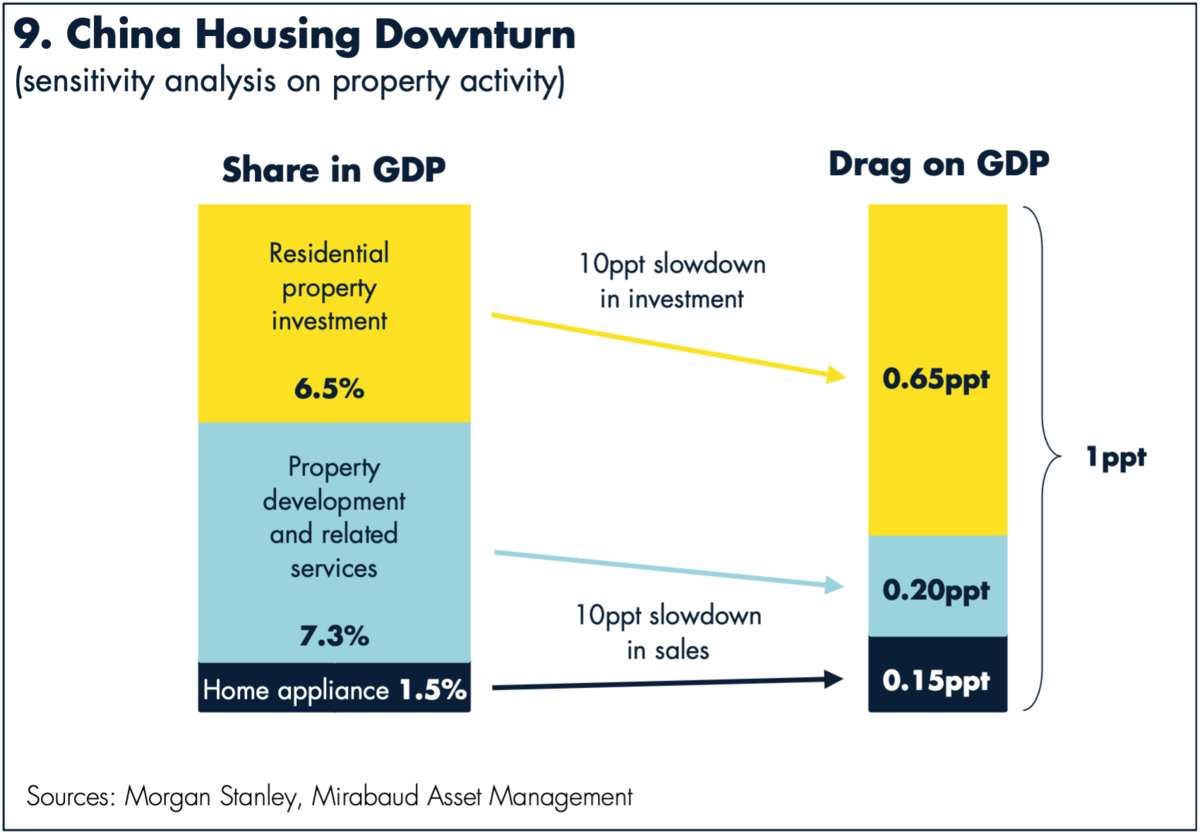

9: Jitters in Chinese real estate

Summer 2021’s wobble in China’s vast property sector was one of the biggest non-Covid stories of 2021.

While the disaster of Evergrande’s complete collapse and subsequent systemic contagion was avoided, the downturn in real estate in the People’s Republic is nevertheless acting as a weight on growth.

2022, however, is set to see both the Winter Olympics and the highly significant 20th Party Congress, both events during which the government will be keen to maintain its prestige in the eyes of the world, meaning it is likely to offer the embattled sector significant support.

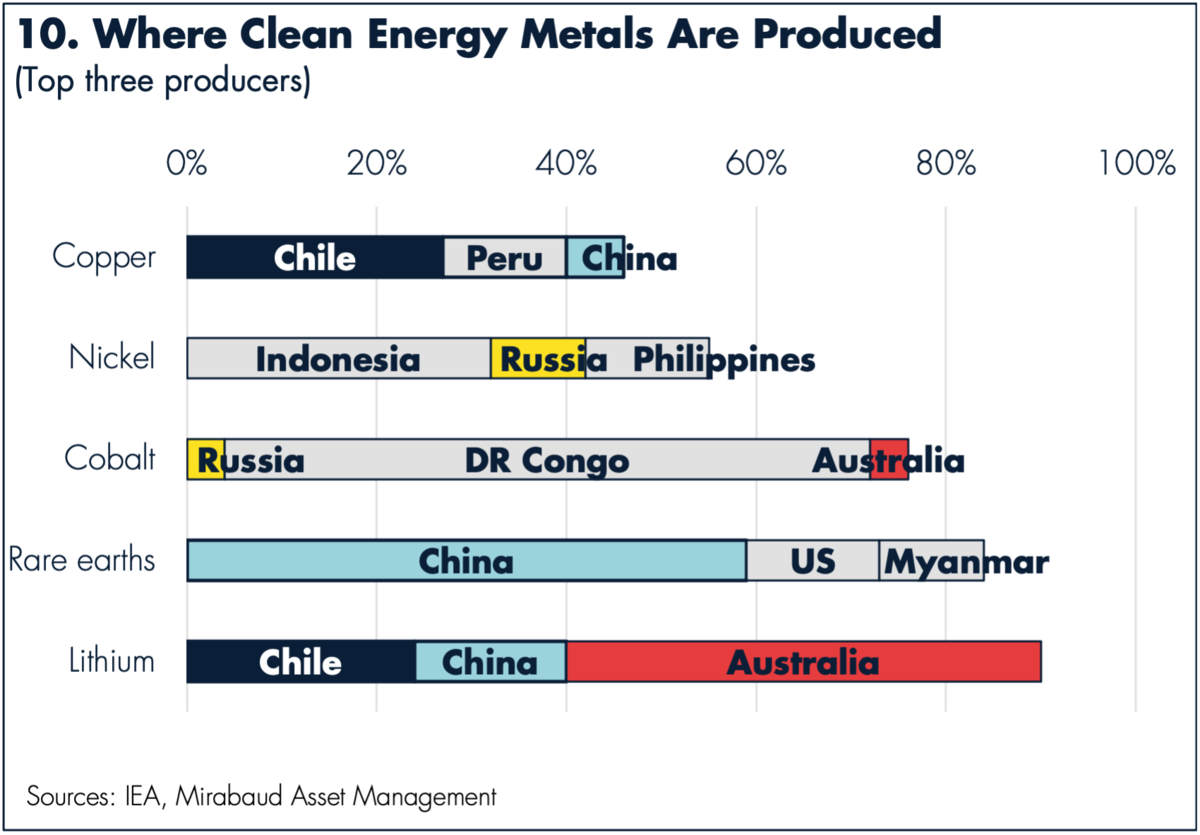

10: Mapping a greened world

If anything, Covid has demonstrated just how vulnerable human societies and economic activity are to environmental factors we cannot control. It has also coincided with the move of environmental concerns to the top of many investors’ minds.

To begin charting the contours of the global economy the transition to a low-carbon energy complex will create, we can look at the key producers of the resources required in clean energy technologies.

Note how concentrated the production of these key commodities is.

11: Carbon isn’t going fast

November’s COP26 Summit in Glasgow saw a great deal of lofty rhetoric from national leaders, but the road to a sustainable energy mix in the developed road is very, very long.

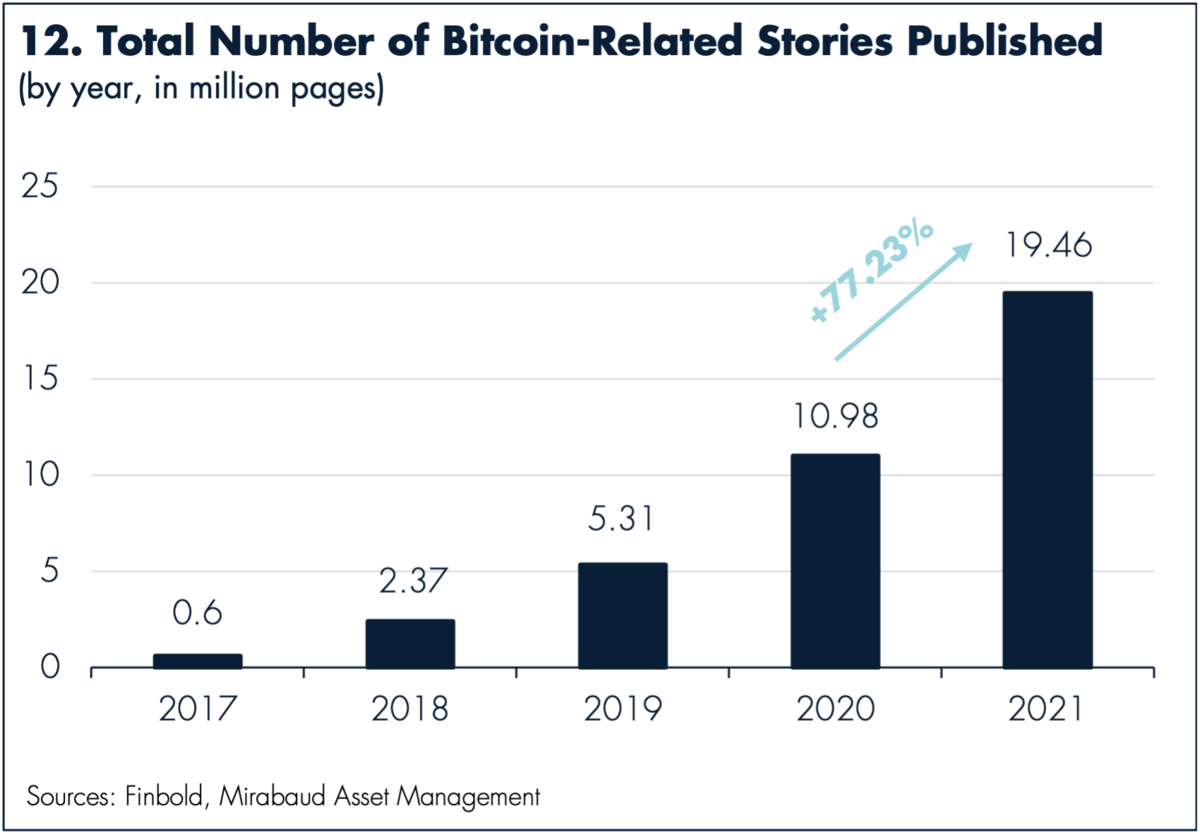

12: Crypto tiptoes to mainstream

2021 saw a growing number of institutional investors start taking cryptocurrencies seriously as an asset class.

Are they the route to a radically rewired global financial system, as some advocates claim? Or are they interesting speculative assets, but little more than technological curiosities?

We have no way of knowing, but on one indicator at least, crypto is at an all-time high:

IMPORTANT INFORMATION

This marketing material is for your exclusive use only and it is not intended for any person who is a citizen or resident of any jurisdiction where the publication, distribution or use of the information contained herein would be subject to any restrictions. It may also not be copied or transferred.

This material is provided for information purposes only and shall not be construed as an offer or a recommendation to subscribe, retain or dispose of fund units or shares, investment products or strategies. Potential investors are recommended to seek prior professional financial, legal and tax advice. The sources of the information contained within are deemed reliable. However, the accuracy or completeness of the information cannot be guaranteed and some figures may only be estimates. In addition, any opinions expressed are subject to change without notice.

All investment involves risks, returns may decrease or increase because of currency fluctuations and investors may lose the amount of their original investment. Past performance is not indicative or a guarantee of future returns.

This communication may only be circulated to Eligible Counterparts and Professional Investors and should not be circulated to Retail Investors for which it is not suitable.

Issued by: in the UK: Mirabaud Asset Management Limited which is authorised and regulated by the Financial Conduct Authority; in Switzerland: Mirabaud Asset Management (Suisse) SA, 29, boulevard Georges-Favon, 1204 Geneva, as Swiss representative. Swiss paying agent: Mirabaud & Cie SA, 29, boulevard Georges-Favon, 1204 Geneva. In France: Mirabaud Asset Management (France) SAS., 13, avenue Hoche, 75008 Paris. In Spain: Mirabaud Asset Management (España) S.G.I.I.C., S.A.U., Calle Fortuny, 6 - 2ª Planta, 28010 Madrid. In Luxembourg: Mirabaud Asset Management (Europe) SA, 25 avenue de la Liberté, L-1931 Luxembourg.

Continue to