Our sustainability beliefs

The financial industry is playing catch up. We have moved from an investment world where Social and Responsible Investing (SRI) was present but more niche to one where it has accelerated into mainstream investing in little more than a few years via Environmental, Social and Governance investing (ESG). “Sustainability or Environmental Impact” is on everyone’s lips and asset managers (along with most of the investment community) are falling over themselves in trying to outdo the competition in terms of who is “greenest”. How this is done in practice both at a firm level and more widely as an investors is of utmost importance. ESG encompasses Environmental, Social and Governance, so a broad spectrum of indicators that encompasses sustainability within the E and the S. As bond investors, we have historically focused on the S and G, as it applies to how companies run themselves which has been ingrained into our overall credit and risk analysis for many years. Today, it is the sustainable part of SRI and ESG investing that is now more in focus.

What does this really mean for both investors and their clients? How motivated are investors to choose investments for the truly long term and the more holistic outcome of climate reduction, de-carbonisation and ultimately sustainable ESG policies?

Companies know that more ESG focused strategies attract not just outside investment, but also makes their businesses more robust. For investors the choice is clear – this is not a luxury, it is the difference between saving our planet or not, and making sure that companies and indeed countries adhere to certain levels of governance. That may sound dramatic, but the choice really is that stark. Those of us providing investment solutions in this environment have not only to align ourselves with our clients, but also take action to improve the ESG nature of our own businesses. How we improve diversity, carbon footprint and educate our employees to understand what is at stake and why all of this is of the utmost importance, and more importantly measure ourselves on these targets. Merely putting the sustainable badge on a fund is not enough. There have to be credible and robust investment processes in place beyond the marketing hype.

For Mirabaud, we take ESG in all of its forms incredibly seriously and use a blend of SRI exclusion factors and a more flexible transitional ESG approach to investing. As a 200-year-old independent financial group with seven successive generations of family ownership, legacy is all important. This is where our independence and a broader perspective of longer-term sustainable investment themes are aligned. We can truly focus upon the longer-term perspective, seeking to invest in entities that add value over the longer-term by contributing positively to transitioning to a more sustainable business profile. We can concentrate on how we want to position ourselves and more importantly our clients for the future. All three facets of ESG – Environmental, Social and Governance – are equally important.

Green bonds are fixed income assets that are issued to fund projects that have environmental benefits. Since their market inception in 2007, Green Bonds today still only represent a very small percentage of the overall debt market. In 2012, Green Bond issuance only amounted to US$2.6 billion* - in 2021, the market is expecting around US$ 500bn of issuance**. The young nature of the Green Bond market poses some challenges for investors, including inadequate green contractual protection, the quality of reporting metrics and transparency. With no single reporting standard comparability becomes difficult and this is where deep analysis is key. We’ll apply our proprietary analysis to this market, which has been crafted from years of fixed income investing in finding credit opportunities with a responsible investing background.

*https://www.investopedia.com/terms/g/green-bond.asp

**Financial Times, February 2021

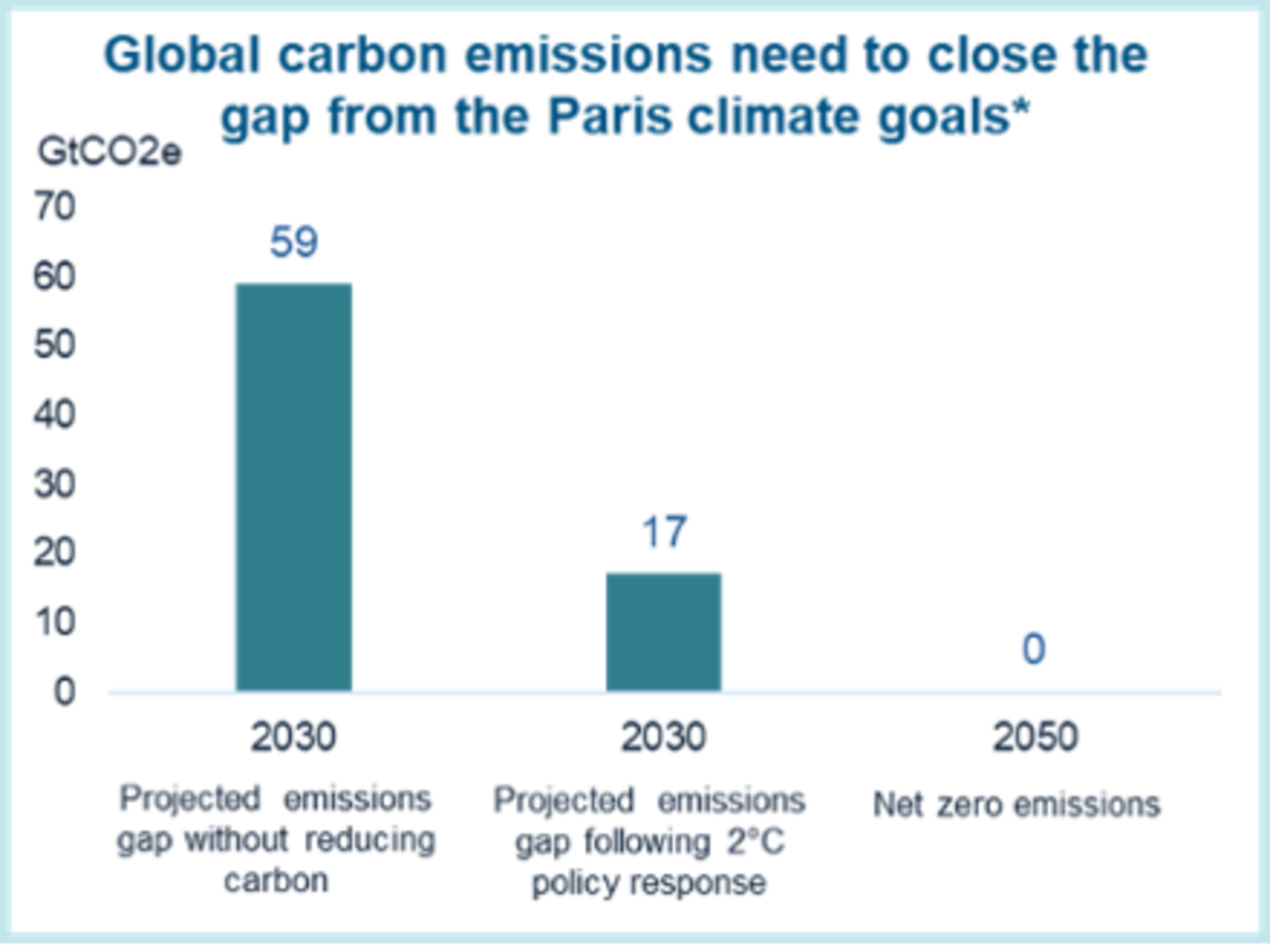

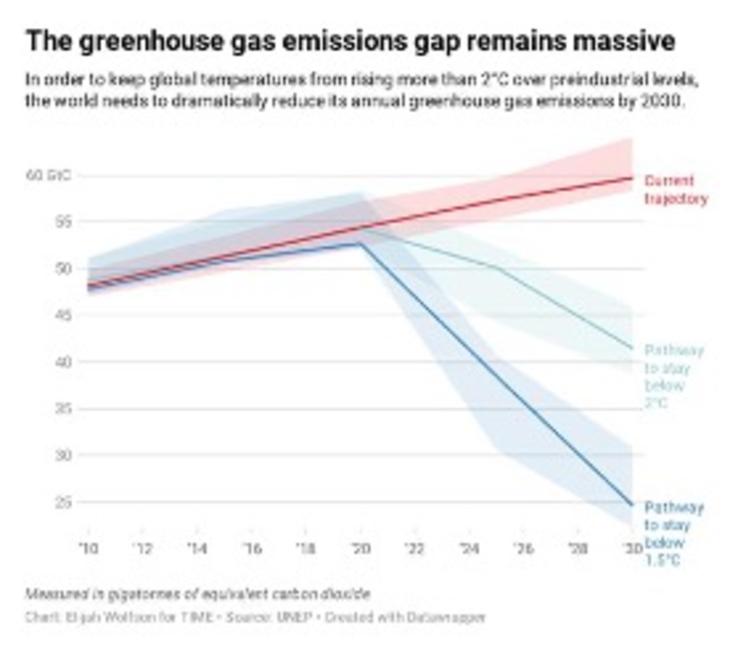

The greenhouse gas emissions gap is significant

Governments around the world have committed to reduce their carbon footprints - more than 50% by 2030 and 100% by 2050 – in line with the Paris Agreement in 2015, which seeks to limit the global temperature rise to a maximum of 2°C above pre-industrial levels. This means significant investment is required by companies to transition towards low carbon. Global spending on the energy transition is also increasing, growing from $297 billion in 2014 to $601 billion in 2020**. As a significant gap still exists with greenhouse gap emissions, this gives rise to significant opportunities in bond issuer that can successfully navigate their transition to low carbon.

Source: *UN Environmental Programme emissions gap report 2018. . **BloombergNEF 2020

Source: IPCC Emissions Scenarios report, 2020

Our focus on climate transition

We are focusing on the all-important thematic of climate change for our Mirabaud Climate Bond Fund. Transition is the key word here. We have to incentivise companies and countries to embark upon this journey. Our fund invests in those entities with explicit net zero targets and/or specific sustainable investment aims through the issuance of green bonds. In addition, we will engage with higher emitters where we feel that there is work to be done and accompanying them to set short, medium and long-term targets.

A clear objective

A climate investment strategy is two-fold; firstly to invest in companies looking to finance overtly sustainable projects, green bonds. Secondly to invest in those companies in transition with the aim to meet the Paris Climate Accords either overtly by design or through other polices. The Paris Climate Agreement states that all signatories (including the USA now) will reduce their carbon footprints by more than 50% by 2030 and by 100% by 2050. The target is to limit global temperature rise to well below 2 degrees Celsius by 2100.

We believe in focusing on the future, investing in companies that are transforming their business model to decarbonise, reach net-zero and meet the Paris objectives, with a target of emissions reduction of 8% per year for the next decade. Entities focused on use of resources, innovating, inventing with this in mind. The challenge of climate change is the single biggest issue we have and links into everything else that is “sustainable”. The warming of our planet is already on an unsustainable path. This is not happening in isolation and will have a significant impact upon our environment, economies and health. De-carbonisation is the primary, if not only solution to arresting global warming.

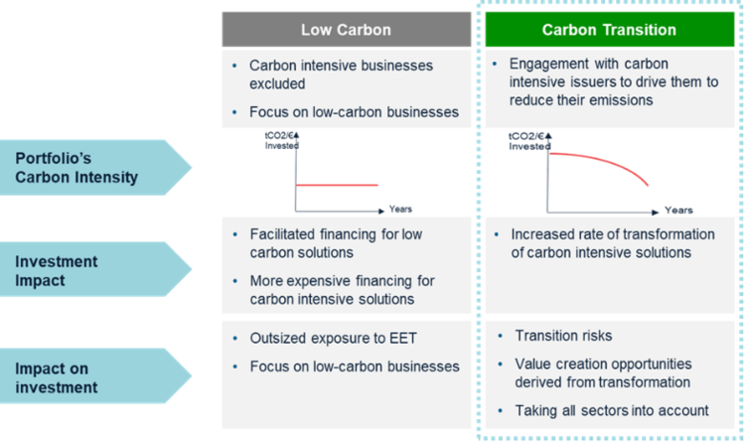

Applying a unique, dual structure

We are taking a differentiated approach to the energy transition. We believe this is best captured through a strategy that has a dual structure of green bonds and corporate bonds.

- We believe that a strategy with a minimum of 51% in labelled green bonds issued explicitly for climate-related and low-carbon investments is an important part of a climate strategy. In this context, proceeds from Green Bond issuance finance projects or activities that promote climate change mitigation, adaption and other environmental purposes, creating the strong climate focus.

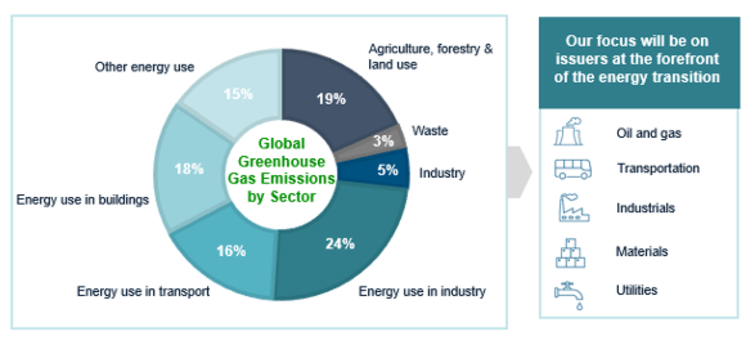

- Issuers that focus on the climate transition are another key area of opportunity. These are issuers that are aligned with or are on track to meet the Paris Climate Accord’s temperature targets. Allocation can be focused around issuers at the forefront of the energy transition in key sectors: Utilities, Oil & Gas, Industrials, Materials and Transportation although this list is not exclusive. These issuers can be high emitters but have shown ambition to decarbonise and/or a commitment to significantly reducing their carbon emissions and environmental impact. Using temperature alignment and historical carbon emissions data, the investment team assigns a colour-coded status to each issuer, which can determine portfolio allocation.

Source: Our World in Data. Total greenhouse gas emissions were 49.4 billion tonnes CO2eq, 2019

Our climate strategy applies an SRI exclusion filter on three primary activities: Controversial weapons, Tobacco and Thermal Coal. The Fund also excludes companies involved in recent major controversies where our engagement policy finds issues. We cross-reference this with Sustainalytics Category 5 controversies.

Our approach to transparency

Transparency is key to this process. We have put in place a rigorous investment process that allows us to look at a wide range of investment opportunities within Fixed Income. We have a longer-term view on transition. The key dates are 2030 and 2050, and we will engage throughout that time period to monitor and challenge companies.

We focus our attention on Green Bonds and Corporate Bonds as our Investment Pool. Green Bonds are those companies seeking to use the proceeds of bond issues for green solutions and projects with clearly defined investment parameters and timelines. Avoiding green washing, maintaining engagement and monitoring progress is key to these investments. The corporate bonds we focus on are those in transition. We identify those issuers at the forefront of net-zero transition. We blend traditional credit analysis with robust ESG analysis when making our investment decision across all opportunities. We also use external tools: Sustainalytics, Trucost, Transition Pathway Initiative, Science Based Targets and Beyond Ratings in conjunction with our own proprietary modelling.

Engagement

Our dialogue and engagement is targeted towards all of investments and aims at encouraging issuers’ decarbonisation, climate target settings and disclosure. We have three primary means of engagement.

- Physical meetings with issuers

- Conference calls to discuss progress and to encourage continuous disclosure and focus on climate action and efforts

- Monitoring of short/medium term greenhouse gas emissions and reduction efforts. Data providers, such as Trucost, update their assessments of companies on an annual basis and we would conduct an annual review of the portfolio as well. We will closely monitor issuers’ climate policies and adapt our assessment based on our engagement and the outcomes of these engagement with issuers, alongside any changes in metrics that occur form the data providers.

We expect enhanced disclosure from issuers around climate change risk mitigation in line with the final recommendations of the TCFD (Task Force on Climate-Related Financial Disclosures), which could be a key requirement for pension schemes. For example, in the UK, pension schemes with assets of £5bn or more have to report on climate risks along TCFD recommendations from October 2021. This will be extended to pension schemes with £1bn or more in assets from October 2022.

IMPORTANT INFORMATION

This fund is not launched therefore all information included herein is subject to change.

This marketing document contains information or may incorporate by reference data concerning certain collective investment schemes ("funds") which are only available for distribution in the countries where they have been registered. This document is for the exclusive use of the individual to whom it has been given and may not be either copied or transferred to third parties. In addition, this document is not intended for any person who is a citizen or resident of any jurisdiction where the publication, distribution or use of the information contained herein would be subject to any restrictions or limitations.

The contents of this document are provided for information purposes only and shall not be construed as an offer or a recommendation to subscribe for, retain or dispose of fund units, shares, investment products or strategies. Before investing in any fund or pursuing any strategy mentioned in this document, potential investors should consult the latest versions of the relevant legal documents such as, in relation to the funds, the Prospectus and, where applicable, the Key Investor Information Document (KIID) which describe in greater detail the specific risks. Moreover, potential investors are recommended to seek professional financial, legal and tax advice prior to making an investment decision.

The sources of the information contained in this document are deemed reliable. However, the accuracy or completeness of the information cannot be guaranteed, and some figures may only be estimates. There is no guarantee that objectives and targets will be met by the portfolio manager.

All investment involves risks. Past performance is not indicative or a guarantee of future returns. Fund values can fall as well as rise, and investors may lose the amount of their original investment. Returns may decrease or increase as a result of currency fluctuations.

This communication may only be circulated to Eligible Counterparties and Professional Investors and should not be circulated to Retail Investors for whom it is not suitable

This document is issued by the following entities: in the UK: Mirabaud Asset Management Limited which is authorised and regulated by the Financial Conduct Authority under firm reference number 122140.; in Switzerland: Mirabaud Asset Management (Suisse) SA, 29, boulevard Georges-Favon, 1204 Geneva, as Swiss representative. Swiss paying agent: Mirabaud & Cie SA, 29, boulevard Georges-Favon, 1204 Geneva. In France: Mirabaud Asset Management (France) SAS., 13, avenue Hoche, 75008 Paris. In Spain: Mirabaud Asset Management (España) S.G.I.I.C., S.A.U., Calle Fortuny, 6 - 2ª Planta, 28010 Madrid. The Prospectus, the Articles of Association, the Key Investor Information Document (KIID) as well as the annual and semi-annual reports (as the case may be), of the funds may be obtained free of charge from the above-mentioned entities.

Andrew Lake

Head of Fixed Income

Continuer vers